How the Wealthy Families Diversify their Wealth & Assets

For decades, many Americans were taught a simple formula for building wealth:

➡️ Buy a house

➡️ Save cash

➡️ Invest in the stock market

➡️ Work hard for 30+ years

But the world’s wealthiest families — the ones operating through “family offices” — think very differently.

And increasingly, Latino entrepreneurs and business owners in America may need to study that model.

Why it matters

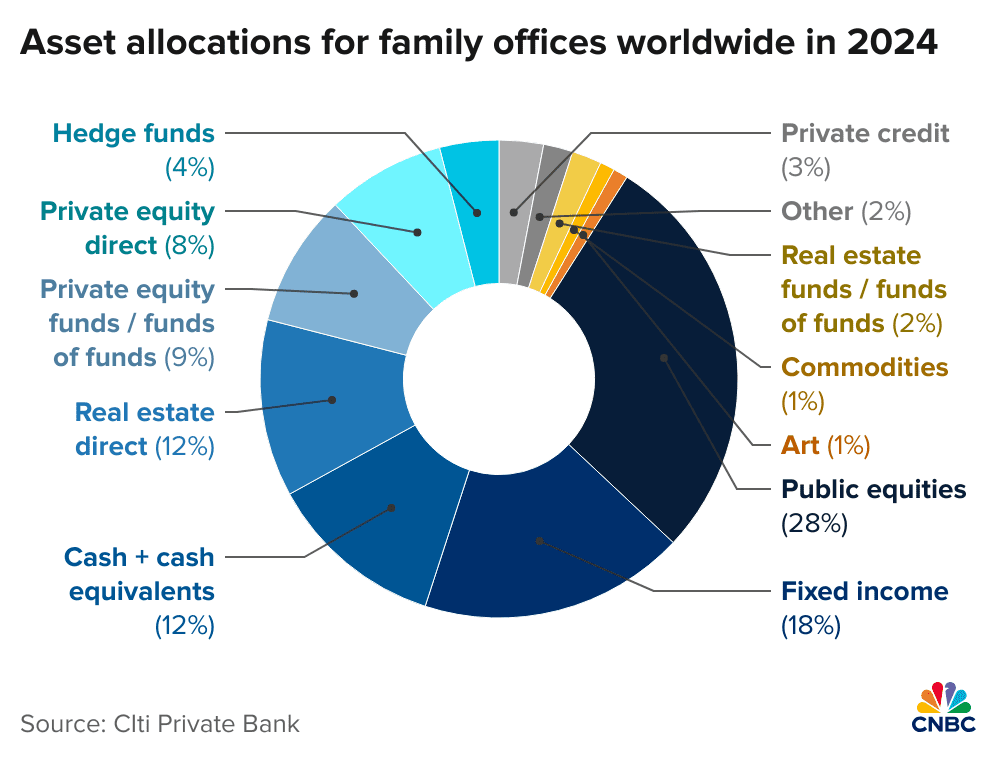

According to data from Citigroup private banking research highlighted by CNBC, family offices globally diversify across many different asset classes — not just stocks.

The typical allocation looks something like this:

- Public equities (28%)

- Fixed income (18%)

- Cash & cash equivalents (12%)

- Direct real estate (12%)

- Private equity (17% combined)

- Hedge funds (4%)

- Private credit (3%)

- Real assets like commodities and art (small allocations)

That diversification is intentional.

The ultra-wealthy are not trying to “hit one home run.”

They are trying to:

- Preserve wealth

- Generate cash flow

- Reduce volatility

- Protect against inflation

- Create multi-generational stability

What exactly is a family office?

A family office is essentially a private financial operation that manages wealth for ultra-high-net-worth families.

Think of it as a combination of:

- Investment firm

- Tax strategy team

- Estate planning office

- Legal department

- Risk management group

- Business advisory firm

Some family offices manage billions of dollars for one family alone.

Examples often include families behind:

- Walmart

- Mars

- Koch Industries

But the core philosophy matters more than the size.

The big lesson: diversification is protection

Many first-generation entrepreneurs concentrate nearly all their wealth into:

- One business

- One property

- One market

- One income stream

That creates massive concentration risk.

If the business slows down, the industry changes, or the economy weakens, the family’s entire financial future can be impacted.

Family offices think differently.

They spread risk across:

- Businesses

- Real estate

- Stocks

- Bonds

- Cash reserves

- Private investments

- Alternative assets

The goal is resilience.

Why this matters for Latino families in America

Many Latino families are entering a new economic era.

Over the last two decades, Latino entrepreneurs have become one of the fastest-growing business segments in the United States. Millions of families are building:

- Tax firms

- Construction companies

- Logistics businesses

- Restaurants

- Insurance agencies

- Real estate portfolios

- E-commerce brands

But building wealth and preserving wealth are two different skills.

That transition — from operator to asset allocator — is where many families either create generational wealth or lose momentum.

The common mistake: staying “cash rich” but asset poor

A lot of small business owners accumulate cash inside:

- Checking accounts

- Low-yield savings

- Idle business accounts

Meanwhile inflation quietly reduces purchasing power.

Family offices typically deploy capital strategically into productive assets designed to:

- Appreciate over time

- Produce income

- Hedge inflation

- Create tax advantages

Examples include:

- Rental real estate

- Index funds

- Private businesses

- Treasury bonds

- Energy infrastructure

- Private credit

- Tax-advantaged retirement structures

Real estate is still important — but not everything

One major takeaway from the chart is that even wealthy families do not put everything into real estate.

Real estate remains important because it can provide:

- Cash flow

- Depreciation benefits

- Inflation protection

- Long-term appreciation

But sophisticated investors also understand liquidity matters.

That is why family offices often maintain:

- Significant cash reserves

- Public market exposure

- Fixed income investments

- Private equity opportunities

Balance matters.

The psychology shift Latino entrepreneurs may need

Many immigrant families were raised with a survival mentality:

- Save cash

- Avoid risk

- Own your home

- Work constantly

But long-term wealth creation often requires a transition toward:

- Asset ownership

- Financial education

- Tax efficiency

- Capital allocation

- Strategic investing

That does not mean reckless speculation.

It means learning how money can work through multiple vehicles simultaneously.

What a modern Latino “family office mindset” could look like

Even without billions of dollars, many affluent Latino families can begin adopting family-office-style thinking:

Step 1: Protect the operating business

The business generates income and opportunity.

Step 2: Build liquidity

Maintain emergency reserves and operational cash flow.

Step 3: Acquire productive assets

Invest in assets that generate income or appreciate.

Step 4: Diversify over time

Avoid having 100% exposure to one industry or one property.

Step 5: Think multi-generationally

Estate planning, trusts, tax strategy, and succession planning become essential.

The bottom line

Family offices are not simply investment vehicles.

They are systems designed to preserve and compound wealth across generations.

For many Latino families in America, the opportunity over the next 20 years may not just be building successful businesses — but learning how to transform business income into diversified, long-term family wealth.

That mindset shift could define the next generation of Latino economic power.