Senator Urges Treasury to Block Undocumented Immigrants From U.S. Bank Accounts

A letter from Tom Cotton to Treasury Secretary Scott Bessent is raising new questions about whether undocumented immigrants could soon face tighter restrictions on access to the U.S. banking system.

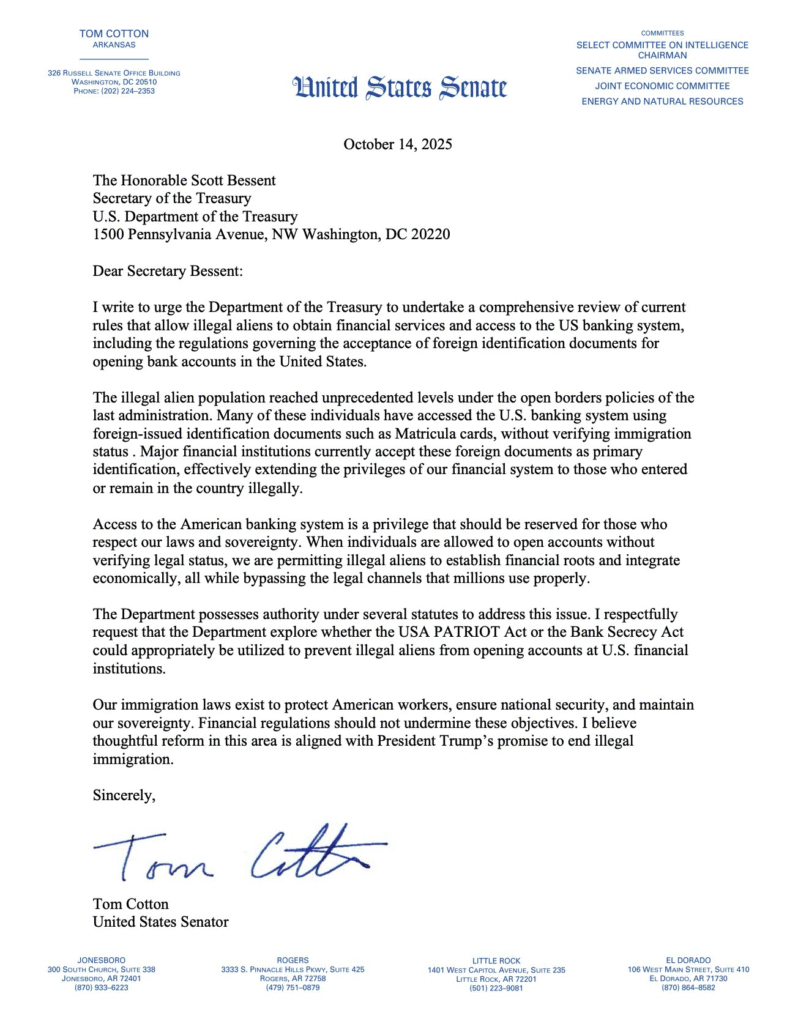

In the October 14 letter, Cotton asks the Treasury Department to review banking regulations that currently allow individuals to open accounts using certain foreign identification documents, including consular IDs such as Mexico’s matrícula card. He argues that access to U.S. financial institutions should be limited to those who are in the country legally and suggests Treasury consider using authorities under the USA PATRIOT Act and the Bank Secrecy Act to restrict access.

While the letter itself does not change policy, immigration advocates and financial experts say it signals a potential shift that could have significant consequences for millions of people.

What Could Change?

Under current federal banking rules, financial institutions must verify a customer’s identity but are not required to verify immigration status. Many banks accept foreign passports, consular identification cards, or Individual Taxpayer Identification Numbers (ITINs) to open accounts.

If Treasury were to reinterpret or revise its guidance:

- Banks could be required to verify immigration status before opening accounts.

- Certain foreign identification documents might no longer be accepted.

- Undocumented immigrants could be barred from accessing checking, savings, or other financial services.

Such changes would likely require regulatory action and could face legal challenges.

Impact on Immigrant Communities

Financial access plays a central role in daily life. Without bank accounts, individuals often rely on cash transactions, check-cashing services, or informal systems that can carry higher fees and greater security risks.

Advocates warn that restricting banking access could:

- Increase reliance on cash, making communities more vulnerable to theft.

- Push workers into unregulated financial services with high fees.

- Make it harder to pay rent, utilities, or taxes electronically.

- Complicate remittances sent to family members abroad.

“This would effectively drive people out of the formal economy,” said one immigrant rights attorney familiar with federal banking compliance policies. “The unintended consequences could be significant.”

Economic Ripple Effects

Undocumented immigrants contribute billions annually in taxes and consumer spending. Many use Individual Taxpayer Identification Numbers to file federal tax returns and pay payroll taxes.

Economists note that removing access to bank accounts could:

- Reduce financial transparency.

- Increase underground economic activity.

- Complicate employers’ payroll processes.

- Create compliance challenges for financial institutions.

Banks themselves may resist sudden regulatory changes, given the operational burden of verifying immigration status — something they are not currently equipped or legally required to do.

Political Context

The letter frames the issue as one of immigration enforcement and national security, aligning with broader efforts to tighten immigration policy. Cotton argues that access to the U.S. financial system should be considered a privilege reserved for those who respect U.S. laws.

The Treasury Department has not publicly responded to the letter.

What Happens Next?

For now, no immediate changes have been announced. Any policy shift would likely involve a formal rulemaking process, giving banks, advocacy groups, and the public an opportunity to comment.

However, immigration policy analysts say the letter may foreshadow broader federal efforts to link financial access more directly to immigration status.

If such changes move forward, millions of immigrants — and the financial institutions that serve them — could face a dramatically altered banking landscape.